It’s easy to mock NFTs (non-fungible tokens),[1] or even to feel cynical about them. Cryptocurrency enthusiasts are spending enough cash to buy a rather nice house, and instead receiving a signed URL for a digital work of art, like this one.

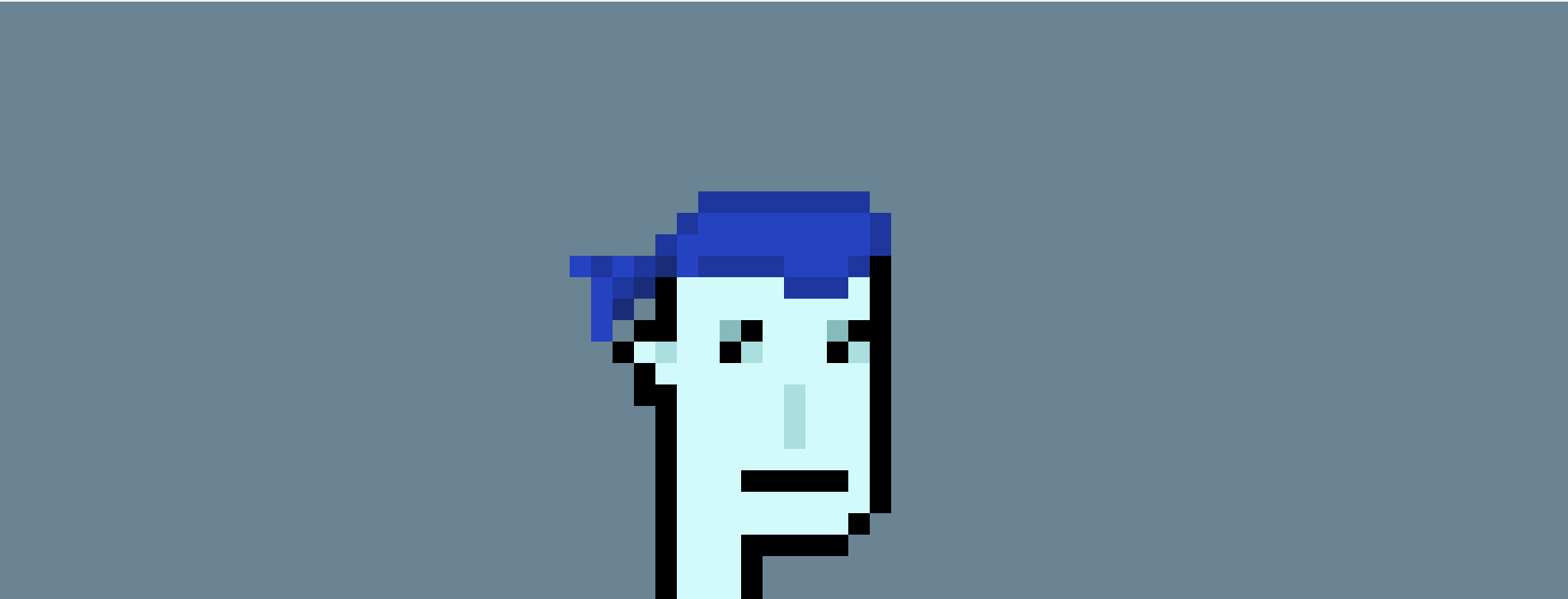

That pièce de résistance is called CryptoPunk 5822. As the name suggests, it is part of an exclusive collection: just 10,000 similar ones exist on the blockchain. Each CryptoPunk is randomly generated, and only 481 of them sport that distinguished bandana, making this one unusually rare. On February 12th, CryptoPunk 5822 sold for 8,000 ETH, or about $24 million.

Similar examples abound: people are paying millions for pixel art and cartoon monkeys. Is this madness, or even a scam? If so then it’s not a new kind of either. It’s not even the first time a pretty penny was spent on thin air. In 1992 sculptor Tom Friedman apparently employed a witch to jinx the space above an empty plinth. The resulting work Untitled (A Curse), which is neither, sold in 2001 for £22,000 (£40,000 today).

Blank canvas and empty space have an august history in the arts, from early 20th century masterpieces like Black Square and White on White, to installations like Air Architecture and Invisible Sculpture, to John Cage’s silent composition 4′33″ (“for any instrument or combination of instruments”). Friedman went on to spend five years producing 1,000 Hours of Staring, a blank piece of paper which he had looked at for a long time. And in parallel with the modern crypto craze, artist Salvatore Garau sold Io Sono, an invisible statue, for $18,000 in 2021. The buyer received a certificate of authenticity.

Though technical skill – or physical existence – may not be a hard requirement for fine art, those naked pedestals are admittedly outliers. Material art commands the biggest price tags, which regularly exceed the $100 million mark, and still dwarf those of blockchain sales.[2] The world’s most valuable artwork, Da Vinci’s Salvator Mundi, sold for $450 million in 2017; the priciest digital piece, Beeple’s Everydays, took a paltry $70 million in 2021. The most celebrated works are both tangible and hard to reproduce, and that seems to make them truly one-of-a-kind. Any pleb can print out CryptoPunk 5822, the magnum opus above. But the Mona Lisa hangs in only one room.

Yet even in the real world, uniqueness is fraught. Forgeries can be good enough to fool expert eyes. And there is plenty of incentive to make them: Han van Meegeren, a right-clicker ahead of his time, sold $250 million (in today’s money) of fakes in the 20th century, reusing old canvases and paint recipes to avoid detection. His copies were so convincing that, after World War II ended, he was arrested on treason charges for selling a Vermeer to Nazi leader Hermann Göring. van Meegeren eventually proved his innocence (and his guilt to the lesser crime of fraud) by making his last forgery in prison.

To avoid being duped like this, the art industry enforces uniqueness (aka non-fungibility) through chains of provenance and forensic techniques. Carbon dating can prove age by the radioactive 14C in organic materials, X-rays can pick up fingerprints, and statistical wavelet analysis can differentiate the hands behind the brushstrokes. But these techniques can still founder with film photography, where copies may be undetectable, and with proverbial Ships of Theseus, artworks which have been so extensively repaired over time that little original material remains. Even where they are effective, those physical signatures are no more tangible than the cryptographic ones used by blockchains. True, pixels are easier to copy than paints. But NFT art is not unique in being reproducible.

In the modern era duplicates are generally thought worthless compared to originals (though there are exceptions: artist Jean-Baptiste-Camille Corot happily signed copies, while the counterfeiter Elmyr de Hory gained such notoriety that his forgeries have been forged). But what makes the difference? Collectors who pay millions for an original painting, instead of a convincing copy, don’t savour the frame’s slightly reduced electron emissions. Perhaps they appreciate the ethereal connection the piece builds to its creator, its self-perpetuating value as a pricey status symbol, or just an ineffable something that the imitations lack. Whatever it is, it is not a material benefit. So why couldn’t virtual ownership provide the same je ne sais quoi?[3]

Token play at that game

NFTs and the art market have much in common, including that they so often resemble self-parody. So apply Sturgeon’s Law: Ninety percent of everything is crap, but the vast quantity of dirt doesn’t negate the gold to be found. It just makes the sieving more rewarding. The human tendency towards pointless (and expensive) fads, not to mention Ponzi schemes, will continue with or without blockchains.

There could be some good news. Artists who tire of brushes and clay have had a tendency to start shitting into containers. (One of 90 cans of Piero Manzoni’s Artist’s Shit sold for €275,000 in 2016, while a Warhol “Piss Painting” fetched $3.4 million. Naturally our buddy Tom Friedman has tried his hand at the medium. Sturgeon applies rather more literally than usual.)

But the new art market might distract the industry from its dirty protest, and encourage a reevaluation of modern tools, media and formats – whether digital brushes, code and generative art, home-made music and videos, animation, memes or manga – that throw down the gauntlet to fine art in more interesting ways.[4] In time some of those media might prove themselves equal to the canvas, in cultural significance as well as in price tags. That would be a break from tradition. But perhaps the idea of art is fungible after all.

“Fungible” basically just means “replaceable”. If you lend me a pound coin, and I send it back to you by wire, you’re not bothered that you didn’t get your coin back: a pound is a pound is a pound. So currency is fungible. But if you lend me the Mona Lisa, you won’t be happy if I return a different painting, a convincing forgery, or even cash. The Mona Lisa is non-fungible: there’s taken to be just one, with no direct equivalent. An NFT is unique in this sense, but rather than being a work of art in itself, it’s like a title deed or certificate that references a (material or digital) work of art. ↩︎

Though the virtual market as a whole is catching up to the material one, at volumes of $41 billion and $64 billion (pre-covid) respectively. ↩︎

Though I’m reminded of Dune: “The power to destroy a thing is the absolute control over it.” For now, digital art lacks this totalitarian sort of ownership. The original piece is publicly available by design, so at best one can only destroy the certificate. In contrast a chaos-loving collector of the classics can hide them away, or burn them all on a whim. If this is partly why the ownership of digital art feels somehow less real, that says a lot about the human psyche. Adding a self-destruct button to an NFT smart contract would certainly be an interesting experiment. ↩︎

If any art software developers are looking for inspiration: I would love to be able to paint digitally and take advantage of HDR on modern (OLED/mini-LED) displays, and I’m even more excited to see what better artists than me could do with that capability. Get to it. ↩︎